I recommend you to check out the latest interview of Melon on RealVision here

As I outlined in my last article on Melon: A turnaround crypto project from the last cycle I think this project weathered the last years of crypto bear market very well and is positioned for major updates along with key contributors like Real Vision and Delphi Research.

Heck, I might even look into launching a Melon Fund on V2 myself as a side project once the investible universe is broadening.

Disclaimer: I personally hold positions in MLN Token.

Assume that the bitcoin cycle plays out close to how it did the last times. Meaning about a 20x from halving in the following 12-18 months. This means you have an incredible return already. However, is that all we can do? Is there a way to increase optionality?

This could also allow you to substitute exposure away from equities and reduce risks, just because we found a more pure play for a potential bull market.

Leveraging without a Margin Call

Brokers let you margin different positions depending on their “risk” assessment. However, it is in the interest of your broker to offer as much margin and leverage as possible. Since most of them are earning on a percentage of total margin volume. I think buying any of these stocks: 12 stocks to research for the next crypto cycle on margin is a bad idea, just because of the volatility involved.

But I found some Call Options with long expiry that I like. With these, there is no chance of a margin call.

MSTR

Dec17’21 220 CALL

RIOT

Jan21’22 7 CALL

list of options with asymmetric upside for a potential 12-18 Month Bull Market

RiskRatcheting

However what if you don’t want all your positions correlated to Bitcoin or Bitcoin Miners? This is why I’m reviewing also different Web3.0 projects like Melon or The Graph.

In addition to the fundamental development of many altcoins, I think they will receive much more awareness once BTC and ETH have shot through their old all-time-highs.

Options of Crypto Tokens

I’m still in search of long-term options on different cryptocurrencies. But I have not found interesting ones yet. Most are either very short-term or not liquid. I mean, who wants to be a call option seller in this environment, hahah? If you know of any platform that I might have missed, let me know: [email protected]

Disclaimer: I own call options on MSTR & RIOT, as well as the crypto tokens MLN & GRT

My Summary: This project has had significant development over this bear market. Key Changes to growth dynamics are imminent but are not at all priced in. Key Question: Will we see AUM Growth?

There are only a few projects that are category creators. Ethereum created the category of Layer 1s with a Virtual Machine running to execute Smart Contracts.

ETHLend or now called Aave was one of the first projects creating the category of lending protocols / crypto money markets

Dfinity created the category of Decentralized Computing Network Protocols

Melon similarly created the category of Asset Management Protocols in 2o17. In that sense, it has been a true pioneer of “Decentralized Finance” long before “DeFi” was established as a term. It has gone through different announcement cycles that influenced the price.

MLN Token Price and Marketcap

However, funds that started using Melon have not seen significant traction. I will give you a review of current developments, token use case and catalysts.

Product/Vision

Melon allows you to outsource all the back office work of a fund for public tokens to its blockchain protocol. Managers can define the asset allocations of Ethereum tokens and the protocol handles new investor deposits, withdrawals, payment of fees, and exchange orders for portfolio positions.

Token

You can invest in the Melon ecosystem by buying the MLN token. There is annual inflation to incentivize developers to improve the protocol. Revenue that is generated from the funds is used to buy back MLN and burn them. This is reducing the MLN supply and a way for token holders to profit from increased usage.

Traction

Currently, there are about 300 funds as well as about 5 Mio USD in total assets within all melon funds. So although the protocol has existed for a few years now, it has not received significant traction with investors. I would argue most of the current volume is people testing the protocol.

Why is that?

Currently, fund managers can only pick out of 10-15 assets for their funds, this is extremely limiting

Funds need to be closed and restarted with protocol updates

Revenue for MLN token holders is not yet on a recurring basis

So, it’s no wonder that MLN barely had any movement yet.

Catalysts

Over the last few months, I’ve followed the changing dynamics within Melon. A lot of the problems above are being addressed. I would advise you to check-out Melon Improvement Proposal #7 along with a financial model for these changes.

Public Equities is one way of playing a crypto bull cycle. It might not have the optionality that Altcoins offer, however, you also encounter fewer risks with regulated company equity than questionable anonymous dev teams with admin keys.

It also offers you the chance to buy on margin or potentially have a better tax structure. But, I’m not here to discuss all advantages or disadvantages. Just wanted to share the list of companies I’m following quite closely.

Since there are only a few of these companies worldwide with limited exchange listings, my guess is, that these will be trading a lot higher than fair value once the bull market is on its way. There is a flood of liquidity chasing growth narratives and only tiny marketcaps to play this theme.

Galaxy Digital Holdings

TSX-V: GLXY

BTC Holdings + Crypto OTC Broker + Crypto VC

Silvergate Capital

NYSE: SI

Crypto Prime Broker

Microstrategy

NASDAQ: MSTR

B2B Software + BTC Holdings

Marathon Patent Group

NASDAQ: MARA

Bitcoin Miner

Hut 8 Mining

NASDAQ: HUTMF

Bitcoin Miner

RIOT Blockchain

NASDAQ: RIOT

Bitcoin Miner

Hive Blockchain Technologies

TSX.V: HIVE

Bitcoin Miner

Bitcoin Group

FRA: ADE

Crypto Exchange + Services

Goldmoney

TSX.V: XAU

Potential Crypto Custodian via Blockvault

TZero

NASDAQ OTC: TZROP

Security Token Exchange

PayPal

NYSE: PYPL

Payment Provider with Bitcoin Revenue

Square

NYSE: SQ

Payment Provider with Bitcoin Revenue

I think there is a case for owning both equities and cryptocurrencies. In the upcoming years, I would assume the choices in public equities become broader.

However, it will see antiquated to buy them with a traditional broker if the rate of Innovation in DeFi keeps up to current levels.

Disclaimer: I own a basket of the first 8 stocks listed in the table. This basket is by far the biggest position in my portfolio.

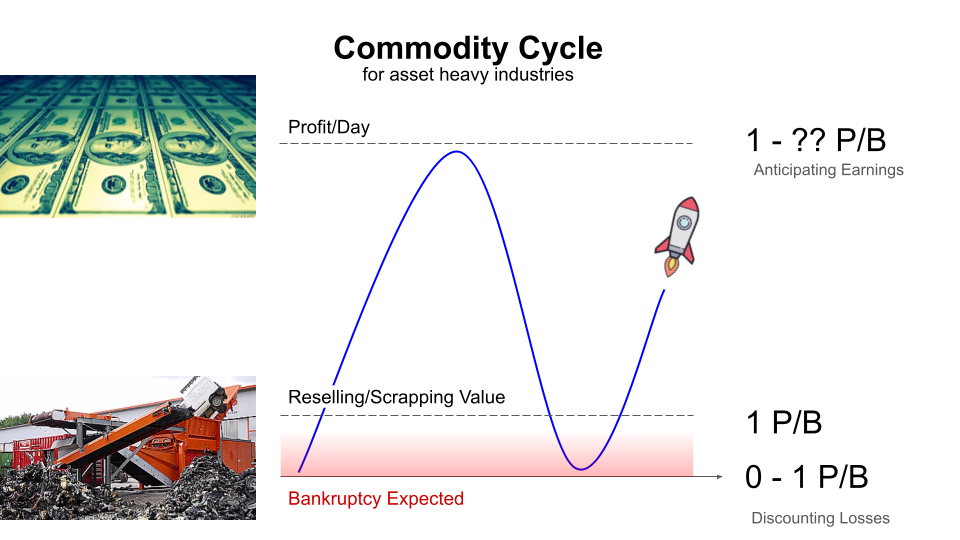

If you look at successful investors, entrepreneurs in the resource sector, they mastered one thing: how to play the resource cycle.

A lot of them even build their life around their industry cycle.

What do I mean by cycle?

Generally, you can cluster companies into two spectrums, brand businesses, and commodity businesses. Commodity businesses don’t necessarily need to be associated with actual resources like e.g. Gold, Oil, Steel. You cluster them because they are dependent on an “industry price” and can not justify a higher price, because their product is mostly indistinguishable from other producers’ products.

A brand however can justify an individual price and is therefore not as dependent on the industry. This description is, of course, over-simplistic but it will help you to understand the commodity cycle.

Let’s make this more specific:

A Bitcoin Miner is a clear commodity business. It is heavily dependent on the current Bitcoin spot price. Users buying Bitcoins don’t care at all from which mining farm it comes from.

A Crypto Newsletter service is heavily dependent on the quality of content, individuals involved, brand and reputation they build. They can however justify a range of prices. This can be considered a brand business.

Now, of course, there is a spectrum in between.

From the investment perspective, brand monopolies are the assets you want to own long-term. They are superb compounders of capital.

Commodity businesses are always subject to price changes for their commodity. This results in burning cash, dilution of shareholders in times when the commodity price is below production cost. On the other hand, once commodity price rises significantly above all-in-sustaining costs, these companies produce high cashflows and often initiate special dividends or buybacks.

Generally, you don’t want to own these assets long-term. However, if you happened to invest in the time of a rising resource price, they are often outperforming brand businesses because their multiples go from “pricing for bankruptcy” to “pricing in daily cashflow”.

So, what’s a commodity cycle?

Historically speaking the commodity cycle is a repeating pattern of a general price increase in energy (e.g. crude oil), industrial metals, precious metals as well as agriculture.

The bull markets for commodities in 1970-75, 1985-90 and 2000-2008 all have been times of high consumer price inflation as well as generally weak for growth equities.

Commodity Index / S&P500

Playing the cycle

Most successful commodity entrepreneurs started their company long into a bear market, waiting for the recovery to set in.

In resources, you are either a contrarian or you are going to be a victim

Rick Rule

Contrarian meaning, they entered the market in years that had the highest bankruptcies. I think in one interview Ross Beaty, a successful mining entrepreneur, joked about: the best time to enter a cyclical industry is when sector ETFs get delisted. For him, this is a contrarian sign that no investor interest is left.

This seems quite straightforward, why wouldn’t anybody do that?

Truth is, that it is hard to raise money in a sector that has been in a bear market for 10-15 years. It’s much easier to do it in times when the same sector equities are trading at all-time high multiples.

How does this apply to Web3.0?

As I already described in Bitcoin Cycles & Narrative Change the halving periods of Bitcoin induced a high price performance over the following 12 – 18 months.

Now, granted, bear markets in crypto have not taken longer than 2-3 years. Not 10-15 years like in physical commodities.

Learning for cyclical markets:

Try to be a contrarian and research projects & teams especially in bear markets

As I described in InvestBasics#3 Narrative it is important to follow the narrative of any investment. Bitcoin is especially interesting in that aspect.

Update: I can recommend checking out this S2F Model with live data for Bitcoin: Digitalik

Bitcoin Stock-to-Flow Model

Bitcoin Cycles

Until now halvings of the block rewards to the miners have been a great leading indicator for 12-18 months of a new bitcoin bull market.

To illustrate, on the day of the first halving in November 2012, the price of one Bitcoin was about $11.50. Over the next 12 months, the price of Bitcoin rose to $270 in late April 2013.

Mitchell Koulouris via Medium

Read a more detailed and great post on bitcoin cycles here by Mitchell Koulouris.

Bitcoins Narrative Change

BTC narratives seem very continuous in the chart. However, if we combine the narratives with financial milestones they look very much like phases with more abrupt transitions:

“Proof of concept” -> after Bitcoin white paper [5]

“Payments” -> after USD parity (1BTC = $1)

“E-Gold” -> after 1st halving, almost gold parity (1BTC = 1 ounce of gold)

“Financial asset” -> after 2nd halving ($1B transactions per day milestone, legal clarity in Japan and Australia, futures markets at CME and Bakkt)

Read a more detailed and great post on that topic here by Nic Carter.

Also, Robert J. Shiller reviews Bitcoins narrative in a historic perspective of other narratives: “Economic Narratives”. Which I can highly recommend.

In 2016 we were 8 years into an equity bull market. Generally, Bear Markets happen every 7-8 years. As I was already working through Monish Pabrais Booklist. It was clear that the best value investors make their most significant decisions for their performance in bear markets.

Monish Pabrai buying Indian Stocks in 2001 after Dot Com Crash

Buffet buying Banking Stocks during GFC in 2008

Buffet buying after the Great Depression of 1930s

So, naturally, I was researching strategies to bridge the time of a market top, or potentially play bear markets. Gold always came up as a crisis investment, however also underperforms in case of a liquidity crunch.

However, also at that time, the narrative of a digital form of Gold emerged. Bitcoin. The digital Gold. Early Youtube videos demonstrated Peer-to-Peer sending. But I didn’t yet understand why it was different from PayPal’s “send to Friends” functionality.

It took another few months and few coincidences for me to learn about Ethereum and that its decentralization offers the chance to move the native currency ETH directly through code.

This pushed me to take a closer look into Bitcoin again. In the rabbit hole, I went …

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.